Mixed Logit (Random Coefficients Logit)#

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pymc as pm

from pymc_marketing.customer_choice.mixed_logit import MixedLogit

from pymc_marketing.paths import data_dir

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [12, 7]

plt.rcParams["figure.dpi"] = 100

%config InlineBackend.figure_format = "retina"

The Mixed Logit model extends the Multinomial Logit (MNL) by allowing random coefficients on alternative-specific covariates, while maintaining fixed population-level effects for individual-specific covariates. It improves on the limitations of MNL by capturing unobserved preference heterogeneity across individuals, but doesn’t require the imposition of market structure assumptions as in Nested Logit models.

This implementation additionally supports a control function approach to endogeneity, allowing potentially endogenous alternative-specific regressors (e.g. price) to be included in a structurally interpretable way.

A defining feature of the model is the explicit decomposition of utility into:

Alternative-specific covariates

Individual-specific covariates

Random effects on alternative-specific covariates

Control function terms correcting for endogeneity

The central idea of Mixed Logit discrete choice models is, as with Nested Logit and Multinomial choice models, to represent an individual’s subjective utility for any good in a marketplace as a function of the observable attributes of that good, while allowing for how individual circumstance and market forces can shift or alter that utility calculation.

Utility Decomposition with Random Effects and Endogeneity Correction#

In the decomposition of the utility metric, we let individual

\(n = 1, \ldots, N \)

choose among alternatives

\( j = 1, \ldots, J \)

at choice occasion

\(t = 1, \ldots, T_n \).

The latent utility for alternative ( j ) is

where:

\(\mathbf{x}_{njt}\): alternative-specific covariates

\(\boldsymbol{\beta}_n\): individual-specific random coefficients

\(\boldsymbol{\alpha} \): fixed coefficients on alternative-specific covariates

\(\mathbf{z}_n\): alternative-specific covariates

\(\boldsymbol{\gamma}_j\): individual-specific coefficients on \( \mathbf{z}_n \)

\(\mathbf{r}_{njt}\): control function residuals

\(\boldsymbol{\lambda_{cf}}\): control function coefficients

\(\varepsilon_{njt} \sim \text{i.i.d. EV}_1\)

Motivation: Control Function for Endogeneity#

Alternative-specific variables such as price may be endogenous due to correlation with unobserved components of utility. Direct inclusion of such variables can bias estimates of both fixed and random coefficients.

The control function approach addresses this by:

Modeling the endogenous regressor in a first-stage equation

Including the resulting residual in the utility function

First-Stage Model#

Let \(p_{njt}\) denote an endogenous alternative-specific regressor (e.g. price). The first-stage model is

where:

\(\mathbf{q}_{njt}\) includes instruments and exogenous controls

\(A\) is a set of instruments for price

\(r_{njt}\) is the first-stage residual

The estimated residual

is carried forward into the choice model.

Second-Stage Utility Adjustment#

The residual enters utility linearly as a control function:

A statistically significant \(\lambda_{cf}\) indicates endogeneity in the original regressor.

This approach preserves the structural interpretation of the utility coefficients while correcting for bias.

Random Effects Specification#

The mixed logit model implements random effects through a hierarchical (multilevel) structure, in which individual-specific coefficients are treated as draws from a common population-level distribution.

For each individual ( n ) and each random coefficient ( k ), the preference parameter is modeled as

The key features of this specification are:

Independence across coefficients

Each random coefficient is assumed to be independent of the others. The joint distribution of the random effects has a diagonal covariance structure.Hierarchical pooling across individuals

Although coefficients are independent across dimensions, they are not estimated independently for each individual. Instead, all individual-level coefficients are linked through shared population-level parameters \(\mu_k\) and \(\sigma_k\).Partial pooling

Individual-level estimates borrow strength from the population distribution. Individuals with limited data are shrunk more strongly toward the population mean, while individuals with richer choice histories exhibit greater dispersion.

This hierarchical structure allows the model to capture systematic preference heterogeneity while remaining computationally tractable and avoiding the complexity of estimating full covariance matrices.

Importantly, while the random coefficients are independent a priori, they may exhibit posterior dependence induced by the data and the structure of the utility function.

Random Effects vs. Endogeneity Control: A Modeling Trade-off#

The mixed logit model combines two powerful mechanisms for explaining variation in observed choices: random coefficients and control functions for endogeneity. While both address sources of unexplained variation in utility, they do so in fundamentally different ways, and understanding the trade-off between them is essential for sound model specification and interpretation.

Random effects explain variation by imposing structure on preferences. By allowing coefficients on alternative-specific attributes—such as price—to vary across individuals, the model attributes persistent differences in behavior to latent taste heterogeneity. In effect, unexplained dispersion in choice behavior is absorbed by assuming that individuals systematically value attributes differently, and that these preferences are stable across repeated choice occasions. This is a structural explanation: variation is interpreted as reflecting genuine differences in preferences.

The control function approach addresses a different source of variation: endogeneity arising from correlation between observed attributes and unobserved utility components. In many choice settings, prices are not set exogenously. They may reflect unobserved product quality, local market conditions, or strategic pricing responses that are also relevant to consumers’ utility. In this case, variation in choices driven by these unobservables should not be attributed to preference heterogeneity. Instead, the control function explicitly removes the component of the endogenous regressor that is correlated with the unobserved utility shock, reallocating that variation away from the structural preference parameters.

When both mechanisms are present, there is an important tension. Random effects are flexible and can “explain away” substantial variation in choices, even when that variation is in fact driven by endogeneity. If prices are endogenous and no control function is included, the model may incorrectly interpret systematic price–utility correlation as evidence of heterogeneous price sensitivity. Conversely, a strong control function can substantially reduce the residual variation attributed to random coefficients, leading to smaller estimated heterogeneity.

The strength and provenance of the pricing instrument therefore play a central role in how variance is partitioned. A weak or poorly motivated instrument may fail to isolate the endogenous component of price variation, leaving the random effects to absorb both true preference heterogeneity and spurious correlation. A strong instrument—one that shifts prices for reasons plausibly orthogonal to consumer utility—allows the control function to explain the appropriate portion of variance, leaving the random coefficients to capture genuine differences in tastes.

From a modeling perspective, this means that random effects and endogeneity controls should not be viewed as substitutes, but as complementary tools with distinct interpretive roles. Random effects encode structural assumptions about preference heterogeneity; control functions encode identifying assumptions about the data-generating process for endogenous regressors. Careful instrument selection and transparent justification are therefore critical, as they directly determine how variation in observed choices is attributed—either to latent preferences or to market-level forces operating outside the utility specification.

In applied work, examining how the estimated heterogeneity changes with and without the control function can be informative. Large shifts in the variance of random coefficients after introducing a valid instrument often signal that what initially appeared to be taste heterogeneity was, in fact, driven by endogeneity.

Travel Choice Example#

Let’s first look at an example of how to implement a Mixed Logit model with out endogeneity correction using PyMC-Marketing. We will use a travel choice dataset that contains information on individuals’ choices among different modes of transportation (car, bus, train, air) along with various attributes of each mode.

data_path = data_dir / "TravelMode_wide.csv"

df = pd.read_csv(data_path)

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 210 entries, 0 to 209

Data columns (total 20 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 individual 210 non-null int64

1 wait_air 210 non-null int64

2 wait_bus 210 non-null int64

3 wait_car 210 non-null int64

4 wait_train 210 non-null int64

5 vcost_air 210 non-null int64

6 vcost_bus 210 non-null int64

7 vcost_car 210 non-null int64

8 vcost_train 210 non-null int64

9 travel_air 210 non-null int64

10 travel_bus 210 non-null int64

11 travel_car 210 non-null int64

12 travel_train 210 non-null int64

13 gcost_air 210 non-null int64

14 gcost_bus 210 non-null int64

15 gcost_car 210 non-null int64

16 gcost_train 210 non-null int64

17 mode 210 non-null object

18 income 210 non-null int64

19 size 210 non-null int64

dtypes: int64(19), object(1)

memory usage: 32.9+ KB

utility_eqs = [

"car ~ wait_car + vcost_car + travel_car | income | wait_car",

"bus ~ wait_bus + vcost_bus + travel_bus | income | wait_bus",

"train ~ wait_train + vcost_train + travel_train | income | wait_train",

"air ~ wait_air + vcost_air + travel_air | income | wait_air",

]

mxl = MixedLogit(

df,

utility_eqs,

depvar="mode",

covariates=["wait", "vcost", "travel"],

)

mxl

<pymc_marketing.customer_choice.mixed_logit.MixedLogit at 0x173d71b50>

The above code block specifies and initializes a mixed logit model for a transportation mode choice problem with four alternatives: car, bus, train, and air. Each string in utility_eqs defines the utility for one transportation mode relative to the baseline alternative. The choice set consists of four mutually exclusive alternatives, and the observed choice is stored in the mode column of the data frame. The baseline alternative is implicitly defined as the last alternative in the list (in this case, “air”).

Alternative-Specific Covariates

The left-hand side of each formula includes alternative-specific attributes:

wait_*: waiting time

vcost_*: variable cost

travel_*: in-vehicle travel time

These variables vary across alternatives and choice occasions and enter utility with fixed population-level coefficients by default.

Individual-Specific Covariates

The middle component of the formula (| income |) specifies income as an individual-specific covariate. Income does not vary across alternatives but shifts the relative utility of each mode through alternative-specific coefficients. This allows income to affect, for example, the attractiveness of air travel differently than car or bus.

Random Effects on Alternative-Specific Covariates

The right-hand side of the formula specifies wait_* as a random coefficient. This means that sensitivity to waiting time is allowed to vary across individuals: The random effect applies only to the alternative-specific waiting-time variables and is constant across all choice occasions for a given individual. Other alternative-specific covariates (vcost_* and travel_*) are treated as fixed effects.

mxl.sample(

fit_kwargs={

"target_accept": 0.95,

"tune": 2000,

"draws": 5000,

"chains": 4,

"cores": 4,

"nuts_sampler": "numpyro",

}

)

Sampling: [alphas_, betas_fixed_, betas_non_random, likelihood, mu_random, sigma_random, z_random]

Sampling: [likelihood]

<pymc_marketing.customer_choice.mixed_logit.MixedLogit at 0x173d71b50>

The Model Graph

We can visualize the model structure using Graphviz to see how the components relate to each other:

pm.model_to_graphviz(mxl.model)

This table summarizes posterior estimates from a mixed logit model with alternative-specific intercepts (alphas), fixed coefficients on alternative-specific covariates (betas_non_random) and the hierarchical random coefficients on waiting time (mu_random, sigma_random).

az.summary(

mxl.idata, var_names=["alphas_", "betas_non_random", "mu_random", "sigma_random"]

)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| alphas_[car] | -8.141 | 2.224 | -12.302 | -4.087 | 0.065 | 0.054 | 1264.0 | 1314.0 | 1.0 |

| alphas_[bus] | 1.404 | 1.351 | -0.979 | 4.126 | 0.027 | 0.021 | 2446.0 | 2353.0 | 1.0 |

| alphas_[train] | 3.409 | 1.297 | 1.090 | 5.919 | 0.028 | 0.019 | 2249.0 | 2437.0 | 1.0 |

| alphas_[air] | -0.063 | 4.916 | -9.617 | 8.763 | 0.058 | 0.083 | 7247.0 | 3148.0 | 1.0 |

| betas_non_random[vcost] | -0.008 | 0.012 | -0.030 | 0.016 | 0.000 | 0.000 | 3248.0 | 2504.0 | 1.0 |

| betas_non_random[travel] | -0.007 | 0.002 | -0.011 | -0.004 | 0.000 | 0.000 | 2333.0 | 2356.0 | 1.0 |

| mu_random[wait] | -0.207 | 0.041 | -0.282 | -0.135 | 0.001 | 0.001 | 863.0 | 1073.0 | 1.0 |

| sigma_random[wait] | 0.124 | 0.037 | 0.064 | 0.198 | 0.001 | 0.001 | 677.0 | 999.0 | 1.0 |

For example if we see alphas_[car] implies a strongly negative mean (−8.18) with a tight credible interval well below zero, which imples that after accounting for wait time, travel time, cost, and income, car is substantially less preferred relative to the baseline. While betas_non_random_[vcost] shows a negative mean (−0.007), indicating that higher variable costs decrease utility across all individuals on average, as expected. While the random coefficient on wait time (mu_random_[wait] and sigma_random_[wait]) indicates that, on average, individuals dislike longer wait times (mean of −0.208), there is considerable heterogeneity in this preference (standard deviation of 0.12), suggesting that some individuals are much more sensitive to wait times than others. The model samples well and effects seem well identified.

High level, this suggests that train is structurally preferred while car is strongly disfavored, and wait time is an important driver of choice with meaningful individual differences.

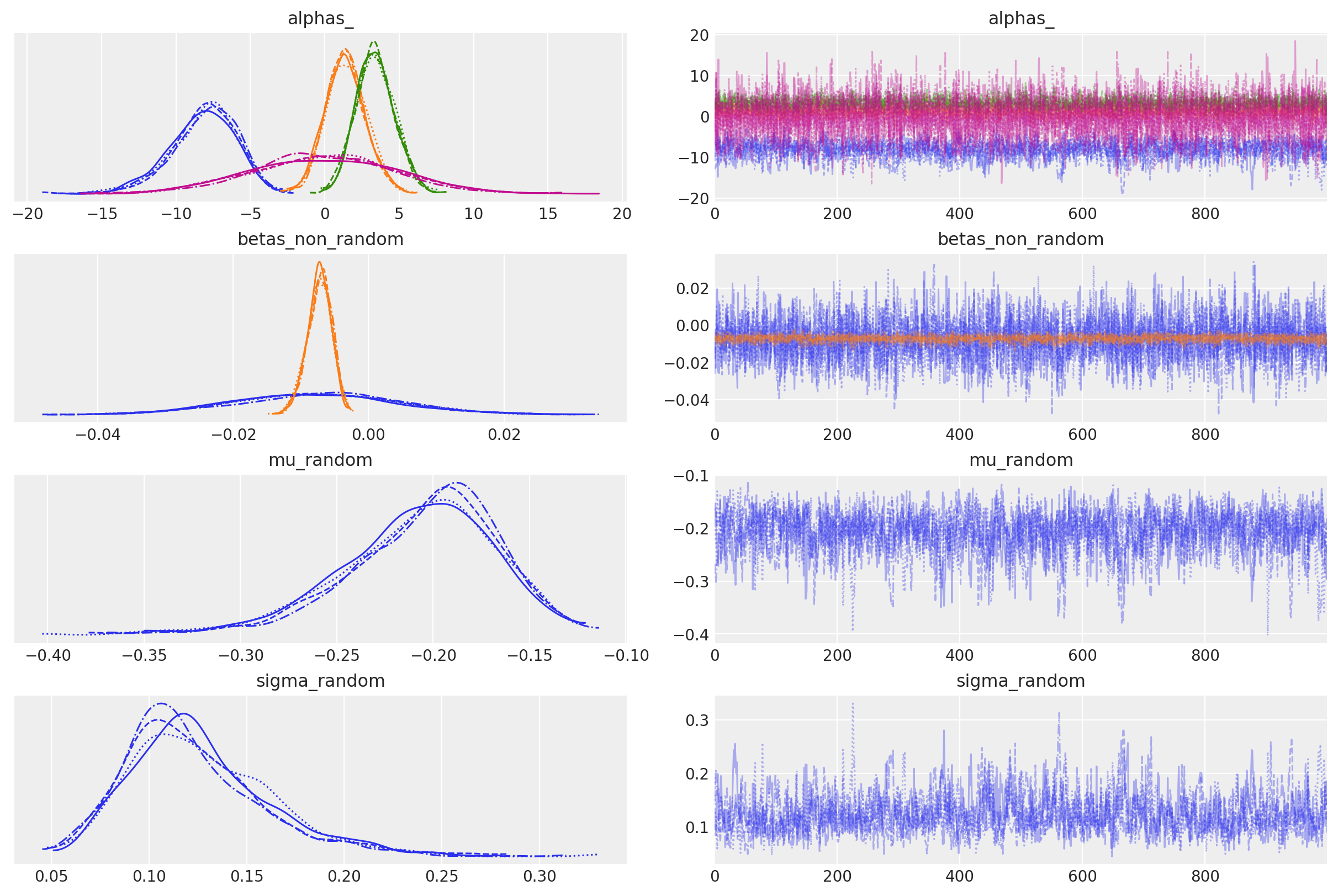

az.plot_trace(

mxl.idata, var_names=["alphas_", "betas_non_random", "mu_random", "sigma_random"]

);

The combination of a negative mean and a nontrivial standard deviation implies that aiting time is a key driver of choice, average disutility is strong and individual differences matter meaningfully.

Counterfactual Analysis#

We can use the fitted mixed logit model to perform counterfactual analysis by simulating changes in choice probabilities under different scenarios. For example, we can analyze how reducing wait times for bus and train while increasing wait time for air travel affects market shares. Similar to the MNL and Nested Logit examples, we first create a new dataset reflecting the policy change, then use the model to predict choice probabilities under this new scenario. Let’s simulate a scenario where wait times for bus and train are halved, while wait time for air travel is increased by 50%.

### Counterfactual Imputations

new_df = df.copy()

new_df["wait_bus"] = new_df["wait_bus"] * 0.5

new_df["wait_train"] = new_df["wait_train"] * 0.5

new_df["wait_air"] = new_df["wait_air"] * 1.5

idata_new_policy = mxl.apply_intervention(new_choice_df=new_df)

idata_new_policy

Sampling: [likelihood]

-

<xarray.Dataset> Size: 34MB Dimensions: (chain: 4, draw: 1000, obs: 210, alts: 4) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 5 6 7 ... 993 994 995 996 997 998 999 * obs (obs) int64 2kB 0 1 2 3 4 5 6 7 ... 203 204 205 206 207 208 209 * alts (alts) <U5 80B 'car' 'bus' 'train' 'air' Data variables: p (chain, draw, obs, alts) float64 27MB 0.06479 ... 2.494e-08 likelihood (chain, draw, obs) int64 7MB 1 2 2 0 0 2 2 2 ... 1 1 1 1 1 2 2 1 Attributes: created_at: 2026-01-19T17:56:48.306500+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 -

<xarray.Dataset> Size: 3kB Dimensions: (obs: 210) Coordinates: * obs (obs) int64 2kB 0 1 2 3 4 5 6 7 ... 203 204 205 206 207 208 209 Data variables: likelihood (obs) int64 2kB 0 0 0 0 0 2 3 0 0 0 0 ... 3 1 0 1 1 1 0 3 1 0 0 Attributes: created_at: 2026-01-19T17:56:48.309613+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 -

<xarray.Dataset> Size: 25kB Dimensions: (obs: 210, alts: 4, covariates: 3, fixed_covariates: 1) Coordinates: * obs (obs) int64 2kB 0 1 2 3 4 5 6 ... 204 205 206 207 208 209 * alts (alts) <U5 80B 'car' 'bus' 'train' 'air' * covariates (covariates) <U6 72B 'wait' 'vcost' 'travel' * fixed_covariates (fixed_covariates) <U6 24B 'income' Data variables: X (obs, alts, covariates) float64 20kB 0.0 10.0 ... 140.0 y (obs) int32 840B 0 0 0 0 0 2 3 0 0 0 ... 0 1 1 1 0 3 1 0 0 W (obs, fixed_covariates) float64 2kB 35.0 30.0 ... 70.0 Attributes: created_at: 2026-01-19T17:56:48.311525+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0

mxl.calculate_share_change(mxl.idata, idata_new_policy)

| policy_share | new_policy_share | relative_change | |

|---|---|---|---|

| product | |||

| car | 0.282359 | 0.087367 | -0.690582 |

| bus | 0.143026 | 0.278940 | 0.950275 |

| train | 0.299637 | 0.514326 | 0.716497 |

| air | 0.274979 | 0.119367 | -0.565903 |

As we would expect, reducing wait times for bus and train increases their market shares, while increasing wait time for air travel decreases its share. The mixed logit model captures these changes while accounting for individual-level preference heterogeneity, providing a nuanced understanding of how policy interventions impact choice behavior across the population. In particular, the model allows us to see how different segments of the population respond differently to changes in wait times, reflecting the underlying heterogeneity captured by the random coefficients. The inference supported here depends strongly on the stability of the preference orderings in the market.

In a behavioral counterfactual, we ask: Holding the estimated utility function fixed, how would predicted choices change if an attribute took on a different value? This interpretation is valid only if the attribute being manipulated is exogenous—that is, if it is uncorrelated with the unobserved determinants of utility. When this condition holds, the estimated coefficient represents a causal marginal effect, and counterfactual simulations can be interpreted causally.

The Threat of Price Endogeneity#

Endogeneity arises when an observed attribute—such as price—is correlated with unobserved components of utility. In demand settings, prices often reflect factors like product quality, brand positioning, local market conditions, or firm strategies that are not fully observed by the analyst but are observed (at least partially) by consumers. By combining mixed logit models with an explicit endogeneity correction, we retain the strengths of rich behavioral modeling while ensuring that counterfactuals correspond to credible causal interventions. In the next section, we show how the control function approach integrates naturally into the mixed logit framework, allowing causal counterfactual analysis without sacrificing flexibility or interpretability. The control function approach can generally be thought of as a instrumental variables strategy adapted to the discrete choice context, providing a principled way to address endogeneity while preserving the behavioral richness of mixed logit models.

To demonstrate this we will need a valid instrument for price in the travel mode choice dataset. Potential instruments could include variables like fuel prices, distance to nearest airport, or regional economic indicators that affect prices but are plausibly exogenous to individual utility. But as we don’t have data to hand on such instruments we will force the issue by simulating an instrumental variable relationship and the re-estimate the mixed logit model with endogeneity correction to show how this works in practice.

X_instruments = np.column_stack(

[df[["gcost_car", "gcost_bus", "gcost_train", "gcost_air"]].values]

)

y_price = df[["vcost_car", "vcost_bus", "vcost_train", "vcost_air"]].values

instrumental_vars = {

"X_instruments": X_instruments,

"y_price": y_price,

"diagonal": True,

}

mxl_1 = MixedLogit(

df,

utility_eqs,

depvar="mode",

covariates=["wait", "vcost", "travel"],

instrumental_vars=instrumental_vars,

)

X, F, y = mxl_1.preprocess_model_data(df, utility_eqs)

Having created our “instrument data”, we will feed it through the model without observing the choice data y, then we will forward sample the model to obtain synthetic choices under a particular regime where the variance can be decomposed into preference heterogeneity and endogeneity components.

model_unobserved = mxl_1.make_model(mxl.X, mxl.F, mxl.y, observed=False)

pm.model_to_graphviz(model_unobserved)

Now we forward sample from the model to obtain synthetic choices under the new regime.

p_obs_samples = np.random.normal(size=(df.shape[0], 4))

alphas_ = mxl.idata["posterior"]["alphas_"].mean(dim=["chain", "draw"])

z_random_ = mxl.idata["posterior"]["z_random"].mean(dim=["chain", "draw"])

# Generating data from model by fixing parameters

fixed_parameters = {

"alphas_": alphas_.values,

"gamma": np.array([[0.5, 0.5382352, 0.51, 0.5]]),

"gamma_0": [1.4, 5.9, 3.2, 0.1],

"lambda_cf": [0.3, 0.3, 0.3, 0.3],

"mu_random": np.array([-0.5]),

"sigma_random": np.array([0.1]),

"sigma_eta": 1.0,

"betas_non_random": np.array([-0.8, 0.4]),

"z_random": z_random_.values,

"P_obs": p_obs_samples,

}

with pm.do(model_unobserved, fixed_parameters) as synthetic_model:

idata = pm.sample_prior_predictive(

random_seed=1000,

) # Sample from prior predictive distribution.

synthetic_y = idata["prior"]["likelihood"].sel(draw=0, chain=0)

Sampling: [betas_fixed_, likelihood]

With the synthetic choices generated under the new regime, we can now analyze how the inclusion of the control function for endogeneity affects the estimated market shares compared to the original mixed logit model without endogeneity correction. What we’re aiming to see is how the price instrument allows us to disentangle true preference heterogeneity from spurious variation driven by endogenous pricing.

# Infer parameters conditioned on observed data

with pm.observe(model_unobserved, {"likelihood": synthetic_y}) as inference_model:

idata_fixed = pm.sample_prior_predictive()

idata_fixed.extend(

pm.sample(

random_seed=100, nuts_sampler="numpyro", chains=4, draws=1000, tune=2000

)

)

Sampling: [P_obs, alphas_, betas_fixed_, betas_non_random, gamma, gamma_0, lambda_cf, likelihood, mu_random, sigma_eta, sigma_random, z_random]

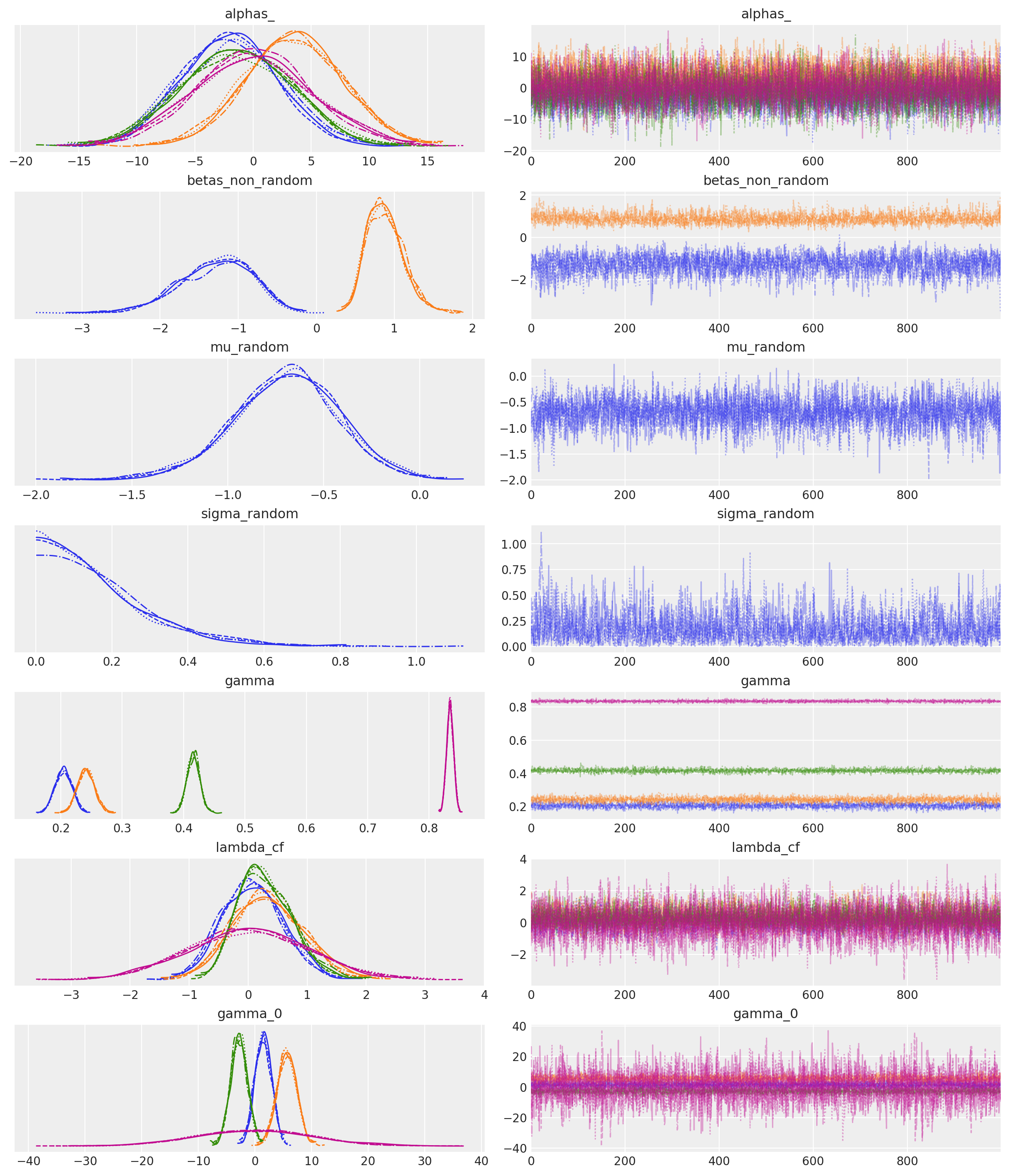

Again, the model samples well and the parameters seem well identified.

az.plot_trace(

idata_fixed,

var_names=[

"alphas_",

"betas_non_random",

"mu_random",

"sigma_random",

"gamma",

"lambda_cf",

"gamma_0",

],

);

However, we can also see how accurately the model recovers the true parameters used to generate the synthetic data. And while the estimates are close, there are some deviations likely due to sampling variability and the complexity of disentangling preference heterogeneity from endogeneity effects. A larger sample size or stronger instruments could help improve recovery of the true parameters.

az.plot_posterior(

idata_fixed,

var_names=["betas_non_random", "mu_random"],

ref_val=list(fixed_parameters["betas_non_random"])

+ list(fixed_parameters["mu_random"]),

);

az.plot_posterior(

idata_fixed,

var_names=["lambda_cf"],

ref_val=list(fixed_parameters["lambda_cf"]),

);

Panel Data and Preference Stability#

Let’s now extend the mixed logit model to handle panel data, where individuals make multiple choices over time. This allows us to capture preference stability and dynamics across repeated choice occasions.

data_path = data_dir / "choice_crackers.csv"

df_new = pd.read_csv(data_path)

last_chosen = pd.get_dummies(df_new["lastChoice"]).drop("private", axis=1).astype(int)

last_chosen.columns = [col + "_last_chosen" for col in last_chosen.columns]

df_new[last_chosen.columns] = last_chosen

df_new.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 3156 entries, 0 to 3155

Data columns (total 20 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 personId 3156 non-null int64

1 disp_sunshine 3156 non-null int64

2 disp_keebler 3156 non-null int64

3 disp_nabisco 3156 non-null int64

4 disp_private 3156 non-null int64

5 feat_sunshine 3156 non-null int64

6 feat_keebler 3156 non-null int64

7 feat_nabisco 3156 non-null int64

8 feat_private 3156 non-null int64

9 price_sunshine 3156 non-null float64

10 price_keebler 3156 non-null float64

11 price_nabisco 3156 non-null float64

12 price_private 3156 non-null float64

13 choice 3156 non-null object

14 lastChoice 3156 non-null object

15 personChoiceId 3156 non-null int64

16 choiceId 3156 non-null int64

17 keebler_last_chosen 3156 non-null int64

18 nabisco_last_chosen 3156 non-null int64

19 sunshine_last_chosen 3156 non-null int64

dtypes: float64(4), int64(14), object(2)

memory usage: 493.3+ KB

Train and Test Split for Panel Data#

We can split the panel data into training and testing sets while ensuring that all choice occasions for a given individual are contained within either the training or testing set. In this way, we can evaluate the model’s predictive performance on unseen individuals while preserving the integrity of the panel structure and assessing preference stability.

utility_formulas = [

"sunshine ~ disp_sunshine + feat_sunshine + price_sunshine | | price_sunshine ",

"keebler ~ disp_keebler + feat_keebler + price_keebler | | price_keebler ",

"nabisco ~ disp_nabisco + feat_nabisco + price_nabisco | | price_nabisco ",

"private ~ disp_private + feat_private + price_private | | price_private ",

]

train_df = df_new[df_new["personChoiceId"] <= 5]

test_df = df_new[df_new["personChoiceId"] > 5]

mxl_panel_train = MixedLogit(

train_df,

utility_formulas,

depvar="choice",

covariates=["disp", "feat", "price"],

group_id="personId",

)

mxl_panel_test = MixedLogit(

test_df,

utility_formulas,

depvar="choice",

covariates=["disp", "feat", "price"],

group_id="personId",

)

We will now train both models.

mxl_panel_train.sample(

fit_kwargs={

"target_accept": 0.95,

"tune": 2000,

"draws": 1000,

"chains": 4,

"cores": 4,

"nuts_sampler": "numpyro",

}

)

mxl_panel_test.sample(

fit_kwargs={

"target_accept": 0.95,

"tune": 2000,

"draws": 1000,

"chains": 4,

"cores": 4,

"nuts_sampler": "numpyro",

}

)

The Model Structure#

We have added multiple observations per individual in the data. This is reflected in the model graph, but we retain only one random effect term on the price coefficient per individual i.e we say that the individual preference is such that it is stable across time.

pm.model_to_graphviz(mxl_panel_train.model)

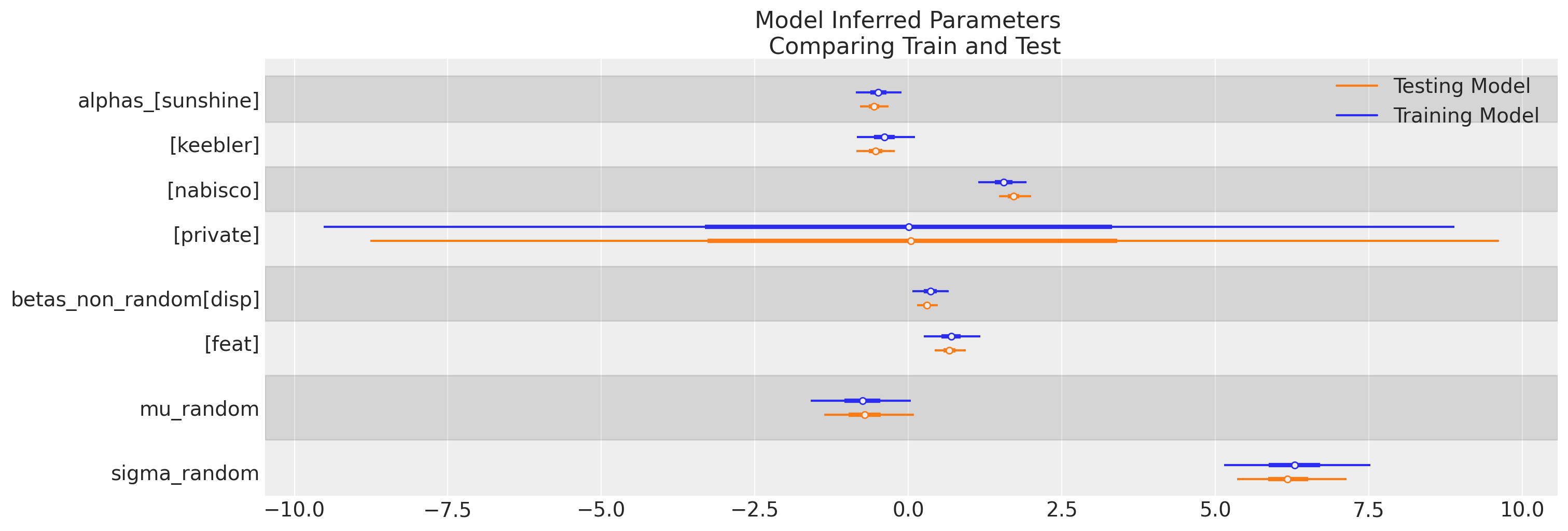

We can observe a broad stability in the model inferred parameters across the train and test splits.

train_inference = az.summary(

mxl_panel_train.idata,

var_names=["alphas_", "betas_non_random", "mu_random", "sigma_random"],

)

test_inference = az.summary(

mxl_panel_test.idata,

var_names=["alphas_", "betas_non_random", "mu_random", "sigma_random"],

)

pd.concat({"train_parameters": train_inference, "test_parameters": test_inference})

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | ||

|---|---|---|---|---|---|---|---|---|---|---|

| train_parameters | alphas_[sunshine] | -0.487 | 0.197 | -0.857 | -0.109 | 0.003 | 0.003 | 3269.0 | 3274.0 | 1.00 |

| alphas_[keebler] | -0.385 | 0.256 | -0.840 | 0.107 | 0.005 | 0.004 | 2652.0 | 3063.0 | 1.00 | |

| alphas_[nabisco] | 1.560 | 0.213 | 1.136 | 1.926 | 0.004 | 0.003 | 2277.0 | 2714.0 | 1.00 | |

| alphas_[private] | 0.029 | 4.947 | -9.521 | 8.901 | 0.050 | 0.110 | 9732.0 | 2335.0 | 1.00 | |

| betas_non_random[disp] | 0.358 | 0.159 | 0.067 | 0.659 | 0.002 | 0.002 | 5090.0 | 3112.0 | 1.00 | |

| betas_non_random[feat] | 0.697 | 0.242 | 0.254 | 1.177 | 0.003 | 0.004 | 6716.0 | 3071.0 | 1.00 | |

| mu_random[price] | -0.745 | 0.436 | -1.586 | 0.042 | 0.007 | 0.006 | 4343.0 | 3355.0 | 1.00 | |

| sigma_random[price] | 6.321 | 0.640 | 5.143 | 7.530 | 0.015 | 0.009 | 1830.0 | 2855.0 | 1.00 | |

| test_parameters | alphas_[sunshine] | -0.554 | 0.125 | -0.788 | -0.324 | 0.003 | 0.002 | 2059.0 | 2811.0 | 1.00 |

| alphas_[keebler] | -0.533 | 0.164 | -0.844 | -0.223 | 0.004 | 0.002 | 1842.0 | 2274.0 | 1.00 | |

| alphas_[nabisco] | 1.717 | 0.138 | 1.482 | 2.001 | 0.003 | 0.002 | 1605.0 | 2062.0 | 1.00 | |

| alphas_[private] | 0.043 | 4.916 | -8.765 | 9.624 | 0.062 | 0.080 | 6397.0 | 2828.0 | 1.00 | |

| betas_non_random[disp] | 0.305 | 0.089 | 0.146 | 0.482 | 0.001 | 0.001 | 6307.0 | 3061.0 | 1.00 | |

| betas_non_random[feat] | 0.673 | 0.137 | 0.428 | 0.940 | 0.002 | 0.003 | 5364.0 | 2932.0 | 1.01 | |

| mu_random[price] | -0.706 | 0.389 | -1.371 | 0.089 | 0.012 | 0.007 | 1038.0 | 1920.0 | 1.01 | |

| sigma_random[price] | 6.199 | 0.482 | 5.353 | 7.143 | 0.018 | 0.008 | 746.0 | 1527.0 | 1.01 |

The same information is probably better reflected in a graph, and we can see how the reference alternative parameters remain unidentified. This is a reminder that discrete choice models estimate relative utility over the baseline private choice.

ax = az.plot_forest(

[mxl_panel_train.idata, mxl_panel_test.idata],

var_names=["alphas_", "betas_non_random", "mu_random", "sigma_random"],

combined=True,

model_names=["Training Model", "Testing Model"],

figsize=(15, 5),

)

ax[0].set_title("Model Inferred Parameters \n Comparing Train and Test");

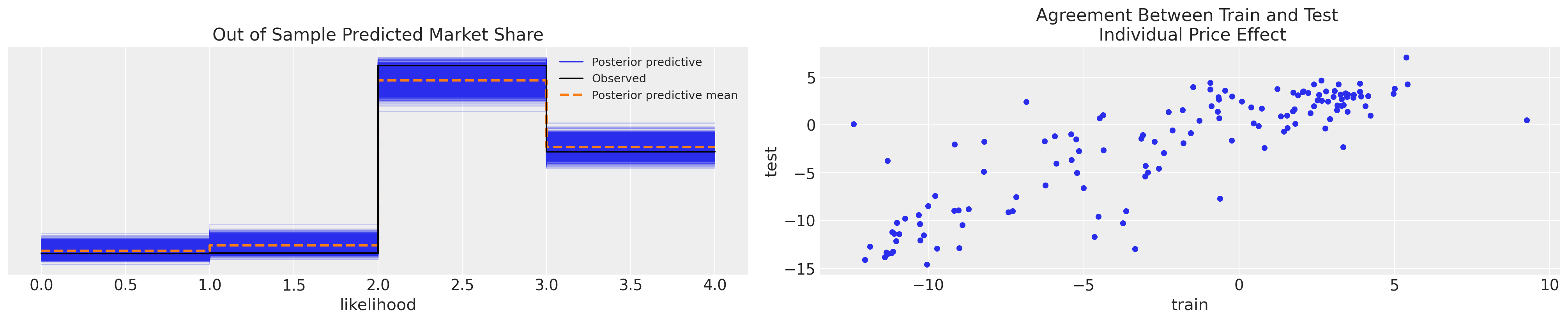

But the real test is whether we can use what we learned about the preference ordering from the consumer’s first five observed choices to predict the market share determined by their subsequent choices. To do this we take our trained model and update the data with the test inputs. We then sample the posterior predictive distribution and evaluate the accuracy of the forecast market share using a posterior predictive check.

with mxl_panel_train.model:

pm.set_data(

{

"X": mxl_panel_test.X,

"y": mxl_panel_test.y,

"grp_idx": mxl_panel_test.grp_idx,

},

coords=mxl_panel_test.coords,

)

idata_predict = pm.sample_posterior_predictive(mxl_panel_train.idata)

Sampling: [likelihood]

These plots confirm a kind of robustness to the individual taste profiles that allow for effect out of sample predictions.

Panel Data and Robust Counterfactuals: How Robust?#

As we’ve seen panel data can play a central role in validating discrete choice models, particularly mixed logit specifications that posit stable, individual-level preference heterogeneity. By observing the same decision-makers across multiple choice occasions, panel data allow the model to distinguish persistent preference orderings from transitory noise. This structure enables out-of-sample prediction at the individual level, providing a meaningful check on whether estimated preferences generalize beyond the estimation sample. When a mixed logit model successfully predicts future choices for the same individuals under new choice situations, it lends credibility to the interpretation that the estimated heterogeneity reflects stable behavioral traits rather than overfitting or incidental correlations.

At the same time, it is important to recognize the limits of what such validation can establish. Strong out-of-sample performance confirms the model’s ability to capture behavioral regularities, but it does not guarantee that the resulting counterfactuals are causally robust. In particular, when market conditions shift in ways that alter the price-setting environment—through policy changes, competitive entry, or supply shocks—the relationship between prices and unobserved attributes may change as well. In such cases, counterfactuals that rely on historically estimated preferences can remain behaviorally coherent yet fail to correspond to the outcomes of feasible market interventions. Panel data strengthen confidence in preference stability, but credible causal counterfactuals still require careful attention to endogeneity and the economic forces that generate prices in the first place. See the work of Train and Petrin in “A Control Function Approach to Endogeneity in Consumer Choice Models” for more details.

Conclusion#

For these reasons, our implementation combines a mixed logit specification with an explicit control function instrumental variables (IV) approach to price endogeneity. The mixed logit component leverages panel data to recover stable, individual-level preference orderings and to support rich behavioral counterfactuals. The control function component, in turn, disciplines the interpretation of price sensitivity by separating exogenous price variation from variation driven by unobserved market forces. Together, these elements allow the model to support counterfactual analysis that is both behaviorally credible and causally interpretable. In particular, the inclusion of a pricing instrument ensures that heterogeneity in price response reflects genuine differences in preferences rather than distortions arising from endogenous price formation, preserving the validity of counterfactual simulations under policy-relevant price changes.

In discrete choice contexts we’re aiming at modelling two mechanisms that either (a) posit robust individual preference or (b) leverage exogenous shocks to solve the simultaneous equations that govern our system, adjusting for unobserved sources of confounding. Causal inference is hard. We are balancing an array of estimation strategies to find and isolate mechanisms that support robust and reliable counterfactual inference. There is no data derived model which will support inference over arbitrarily distant counterfactual scenarios, so we must always attempt to justify the counterfactual argument our model makes!

%load_ext watermark

%watermark -n -u -v -iv -w -p pymc_marketing

Last updated: Mon Jan 19 2026

Python implementation: CPython

Python version : 3.12.12

IPython version : 9.8.0

pymc_marketing: 0.17.1

pandas : 2.3.3

matplotlib : 3.10.8

numpy : 2.3.5

pymc : 5.27.0

arviz : 0.23.0

pymc_marketing: 0.17.1

Watermark: 2.5.0